Crypto Tax Penalty Calculator

Your Tax Liability

It’s 2025, and the IRS isn’t asking nicely anymore. If you’ve made money from Bitcoin, Ethereum, or any other cryptocurrency and didn’t report it, you’re not just risking an audit-you’re risking five years in prison and a $250,000 fine. That’s not a scare tactic. That’s federal law. And the government now has the tools to find every single transaction you ever made-even if you thought it was anonymous.

Why Crypto Is Treated Like Property, Not Cash

The IRS doesn’t see your Bitcoin as money. It sees it as property. That means every time you sell, trade, or spend crypto, you’ve triggered a taxable event. Buy $500 worth of Ethereum. Sell it for $800? You’ve got a $300 capital gain. Pay for coffee with 0.02 BTC worth $70? That’s a $10 gain if you bought it for $60. Even if you just swapped one coin for another, the IRS treats it like selling one asset and buying another. No minimum threshold. Not even $10 is safe from reporting.And here’s the kicker: you have to report every single one of these transactions. Not just the big ones. Not just the ones on Coinbase. Every transfer between your wallets, every staking reward, every airdrop you claimed. The IRS doesn’t care if you used a decentralized exchange or a peer-to-peer trade. If you made a profit, you owe tax.

What Happens When You Don’t Report

Criminal tax evasion isn’t about being sloppy. It’s about intent. If you knowingly hide crypto income, you’re committing a felony. That’s not a civil mistake you can fix with a payment plan. That’s a federal crime with real jail time.The maximum penalty? Five years in federal prison. A $250,000 fine-for individuals. For businesses? Double that. But that’s not all. On top of the criminal fine, you’ll owe:

- Back taxes on all unreported gains

- Interest on those taxes, compounding daily since the original due date

- Up to 75% in civil penalties for fraud

- Additional 25% for failing to file

- Another 25% for failing to pay

So if you owed $10,000 in taxes and hid it, you could end up paying $27,500 in penalties and interest-on top of the $250,000 fine and possible prison time. That’s not a typo. That’s the math the IRS uses.

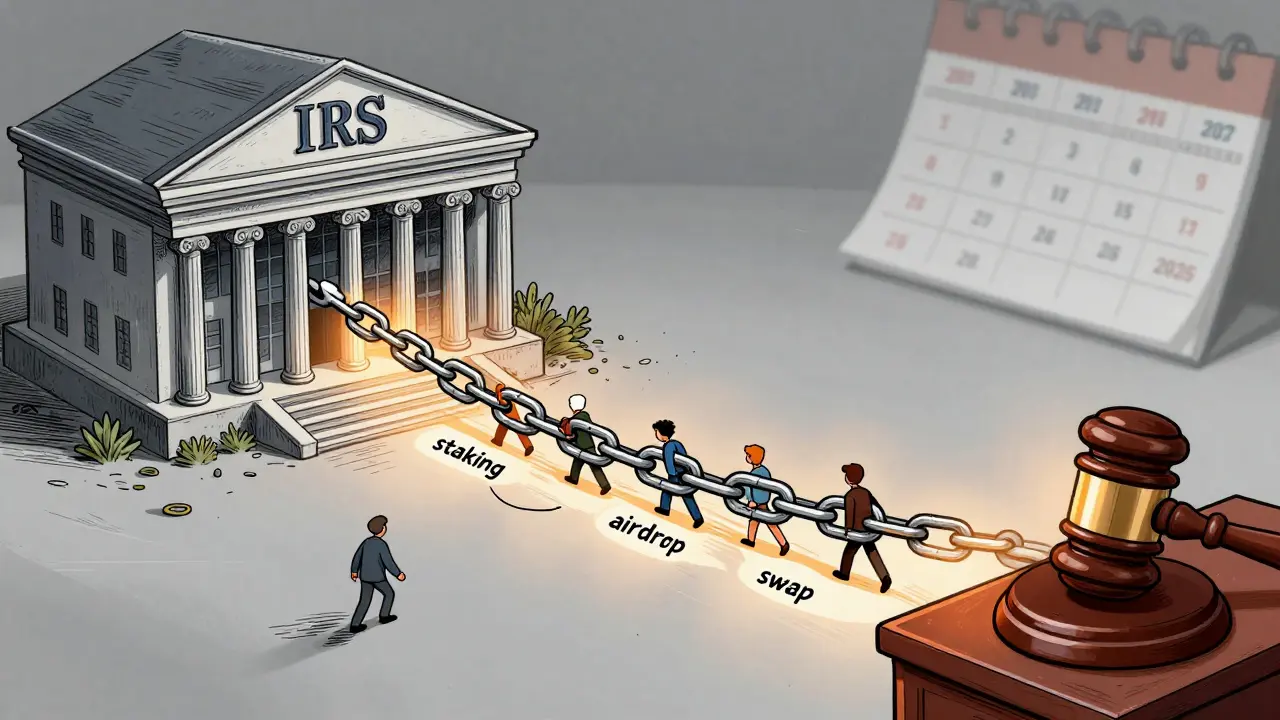

The New Surveillance System: Form 1099-DA

Starting January 1, 2025, every U.S. crypto exchange-Coinbase, Kraken, Binance US, Gemini, you name it-must report your transactions to the IRS using Form 1099-DA. This isn’t like the old 1099-B for stocks. This form tracks every single trade, transfer, and reward. It includes:- Buy/sell dates and prices

- Wallet addresses involved

- Types of digital assets traded

- Cost basis and proceeds for each transaction

Before 2025, the IRS had to guess what you did. Now, they get a full digital ledger of your activity. And they’re not waiting for you to get caught. They’re using blockchain analytics tools like Chainalysis and Elliptic to trace transactions across years-even if you moved crypto to a non-U.S. exchange or used a mixer. Your past is now public record on the blockchain. The IRS can look back five, seven, even ten years.

It’s Not Just Exchanges-Your Wallets Are Tracked Too

You might think, “I moved my crypto to a hardware wallet. They can’t track that.” Wrong. The IRS doesn’t need to know what’s in your wallet. They just need to know where it came from and where it went. If you sent 5 BTC from Coinbase to your Ledger in 2023 and then sold it in 2024, the IRS now has a clear trail: Coinbase reported the withdrawal. Your exchange (or the one you sold on) reported the sale. The math adds up.And starting in 2025, you can’t use the old “universal cost basis” method anymore. You have to track each coin individually-wallet by wallet. That means if you bought Bitcoin at $30,000 in 2021 and another at $45,000 in 2022, you can’t just say, “I sold 1 BTC at $60,000, so my gain is $15,000.” You have to prove which specific coin you sold and what you paid for it. If you can’t, the IRS assumes the highest cost basis-meaning you pay more tax.

Legal vs. Illegal: The Line Between Tax Avoidance and Evasion

There’s a big difference between saving money legally and hiding income illegally.Tax avoidance is smart. You hold crypto for over a year to get lower long-term capital gains rates. You use tax-loss harvesting to offset gains with losses. You contribute crypto to a Roth IRA if your platform allows it. These are legal moves that reduce your tax bill.

Tax evasion is lying. Not reporting staking rewards. Failing to declare airdrops. Pretending you didn’t sell crypto because you “just moved it.” Using a foreign exchange to avoid reporting. That’s fraud. And the IRS treats it like fraud-even if you only evaded $2,000 in taxes.

There’s no “small-time” crypto tax evasion. The law doesn’t care how much you made. It only cares if you tried to hide it.

What People Are Actually Getting Caught For

You think you’re safe because you didn’t make millions? Think again.In 2024, the IRS sent out over 12,000 letters to crypto holders asking them to explain unreported income. Most were for gains under $5,000. One guy in Texas got audited because he sold $1,200 worth of Dogecoin in 2021 and never reported it. He paid $900 in taxes, $700 in penalties, and still got a formal warning letter.

Reddit threads are full of people scared they’ll be next. r/CryptoCurrency and r/tax are flooded with posts like, “I traded crypto in 2018 and forgot to report it-what do I do?” The answer: file an amended return (Form 1040-X) and pay what you owe. Voluntary disclosure often cuts penalties by 50% or more. Wait until the IRS finds you? You’re gambling with your freedom.

Tools That Can Save You

You don’t need to be a tax expert to stay compliant. Tools like Koinly, CryptoTaxCalculator, and CoinLedger connect to your wallets and exchanges, auto-calculate your gains and losses, and generate IRS-ready reports. Most cost under $100 a year. That’s less than most people spend on one crypto trade.These tools don’t just help with 2024. They can import your entire transaction history going back to 2017. If you’ve held crypto for years, they can rebuild your cost basis-even if you lost your spreadsheets. That’s how you prove you’re not hiding anything.

What You Should Do Right Now

If you’ve ever traded, sold, staked, or received crypto and didn’t report it:- Stop ignoring it. The clock is ticking.

- Gather every transaction record you have-exchange statements, wallet exports, screenshots.

- Use a crypto tax tool to calculate your total gains and losses.

- File an amended return (Form 1040-X) for each year you missed.

- Pay what you owe. Interest will keep growing.

Don’t wait for a letter. Don’t hope the IRS forgets. They won’t. The system is built to catch you. And it’s already working.

Global Enforcement Is Only Getting Stronger

The U.S. isn’t alone. In 2024, global crypto tax enforcement hit $5.1 billion in penalties. The U.S. accounted for nearly half of that. Australia, the UK, Canada, and Germany have all ramped up audits and are sharing data with the IRS through international agreements. If you moved crypto overseas to hide it, that’s now a red flag.And the penalties keep rising. The average fine for crypto businesses jumped 21% in 2025. For individuals, the message is clear: compliance isn’t optional. It’s mandatory. And the cost of ignoring it just got a lot higher.

bro i sold 0.5 btc for $30k in 2021 and just forgot about it till last year

thought it was like bartering with friends

now i got a letter and my hands are shaking

im not even rich just dumb

the real tragedy isnt the tax-it’s how the system turns human behavior into accounting problems

we used to trade goods, now we trade digital ghosts and the state demands receipts for every ghost we traded

we’re not criminals, we’re just early adopters who trusted the myth of anonymity

and now the ledger doesn’t forget

i’ve been using koinly since 2022. it’s not perfect but it saved me from panic.

if you’re reading this and haven’t filed-do it before the letter comes.

in india we don’t have crypto tax enforcement yet but i read this and i feel so much empathy for americans

because the fear of being caught is not just about money-it’s about shame, about being labeled a liar when you just didn’t understand

i remember when i first bought btc in 2019, i thought it was like buying gold and storing it in a drawer

no one told me that every time i moved it, it was a taxable event

now i educate my friends, i tell them to keep records, i tell them to use tools

because ignorance is not a defense anymore, and we should not let others suffer the way we did

THE IRS IS A MONSTER THAT EATS PEOPLE WHO DONT REPORT THEIR BITCOIN GAINS

YOU THINK YOU’RE SMART HIDING IT ON BINANCE? LOL

CHAINALYSIS TRACKS YOUR WALLET LIKE A GPS

THEY KNOW YOU BOUGHT 1 ETH AT $1200 AND SOLD IT AT $4200

AND THEY’RE COMING FOR YOU WITH A TAX GUN

AND IF YOU THINK YOU’RE SAFE BECAUSE YOU’RE NOT RICH-THINK AGAIN

THEY AUDITED A GUY WHO MADE $1200 IN DOGECOIN

HE GOT A LETTER

HE PANICKED

HE STILL OWES $1600 IN PENALTIES

YOU THINK YOU’RE DIFFERENT?

YOU’RE NOT

YOU’RE NEXT

you’re not alone. i was terrified too.

but i filed my amended returns last month.

paid what i owed, took the penalty, slept better than i have in years.

the system is brutal but it’s not evil.

it’s just… relentless.

and you don’t fight it by hiding.

you fight it by showing up.

do the thing. it’s not as scary as the fear.

tax evasion isn’t about how much you made. it’s about intent.

if you didn’t know, fix it.

if you knew and lied-that’s on you.

no one owes you anonymity on a public ledger.

my cousin got audited last year for $800 in crypto gains.

ended up paying $2k in penalties.

he cried in front of his kids.

we all thought it was just ‘crypto stuff’.

turns out the IRS doesn’t care what you call it.

they care if you made money and didn’t tell them.

i just checked my old wallet exports.

found 47 transactions i never reported.

some from 2018.

the math is horrifying.

but i’m using crypto tax calculator tonight.

and i’m filing.

not because i’m scared of jail.

because i don’t want to look back and think i cheated my way out of responsibility.

people who evade crypto taxes are just lazy entitled brats who think blockchain is their personal slush fund

you didn’t ‘earn’ crypto-you exploited a loophole that was never meant to last

now the grownups are cleaning up your mess

and you think you deserve sympathy?

get a job and pay your taxes like the rest of us

AMERICA ISN’T EVEN THE WORST

THEY’RE JUST BEING LAZY

IN RUSSIA THEY JAIL YOU FOR 10 YEARS FOR UNREPORTED BITCOIN

AND THEY DO IT WITH A SMILE

THEY’RE NOT EVEN ASKING

THEY JUST TAKE YOUR WALLET AND SEND YOU TO A CELL

SO BE GRATEFUL YOU’RE IN THE U.S.

THEY’LL AT LEAST SEND YOU A LETTER FIRST

LOL

❤️🇺🇸

the blockchain is the ultimate snitch

it doesn’t forget, it doesn’t forgive, it doesn’t care if you cried while you deleted your spreadsheet

every satoshi you moved? logged.

every airdrop you claimed? tracked.

every time you thought you were sneaky?

you were just dancing in a room full of CCTV

and now the cops are knocking

with a subpoena and a calculator

oh sweet jesus another one of you ‘i didn’t know’ people

you had 7 years to learn

you had reddit

you had koinly

you had a google search bar

you chose ignorance over responsibility

now you get to pay for it

and don’t think you’re special because you only made $500

the law doesn’t care about your ‘small-time’ crime

it only cares that you lied

and liars don’t get mercy

my heart goes out to everyone who’s reading this and feeling overwhelmed

you didn’t wake up one day and decide to break the law

you just didn’t know

and now you’re terrified

but here’s the truth-you’re not a criminal

you’re a person who got caught in a system that moved faster than education

so take a breath

gather what you have

use a tool

file what you can

and forgive yourself

the goal isn’t perfection

it’s showing up

and that’s already brave

i’m a software engineer who used to trade crypto on weekends

never thought i’d be filing amended returns at 3am

but i did

and i’m glad i did

because now i sleep without wondering if the IRS is coming

and if you’re reading this and haven’t done it yet

you can too

it’s not easy

but it’s easier than prison